Toolkit: Contribution

Exclusive content on Boosty, video classes on YouTube, summaries and notes on Instagram, units 1~5 content in the best free textbook, class extracts on TikTok, text below. Have fun!

The main purpose of contribution is to manage fixed costs.

Just a reminder to keep a record of all the tools in the table below. As long as you can fill in all the cells of the table, you will be able to write a successful IA.

How to

There is no point in reading further if you do not know or do not remember the types of costs, cost centres and outsourcing. Please check out classes 3.3, 3.9, and 5.4 to review/learn the types of costs, cost centres, and outsourcing.

Contribution is the difference between the selling price and variable costs. In other words, contribution is what has remained to pay for fixed costs. Contribution per unit and total contribution can be calculated using the formulae below:

Contribution per unit = unit price – unit variable cost

Total contribution = total revenue (TR) – total variable costs (TVC)

Total contribution = contribution per unit ⨉ quantity (Q)

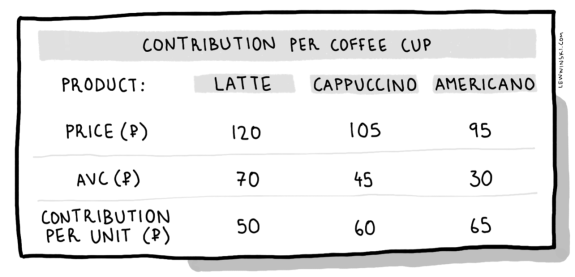

Let’s imagine a school cafeteria is calculating contribution per unit for the three types of coffee it offers. If a cup of cappuccino is priced at ₽105 and variable costs per cup are ₽45, then ₽60 is left to pay fixed costs. See contribution per unit for latte and cappuccino in the table below.

Contribution has many uses. If you have already learnt the entire IB Business Management syllabus, then you should know that contribution is used to calculate break-even quantity, is used to make pricing decisions (including contribution pricing), and is used in product portfolio management.

In addition to the uses identified above, the IB wants you to learn three more:

- contribution costing,

- absorption costing, and

- make-or-buy analysis, which we actually already learnt in 5.6.

Let’s learn these three IB-prescribed uses of contribution.